Last year throughout October I tracked my spendings to get a better picture of where the money is going. And I wanted to repeat it in 2023 as well. Then we had plans of being on vacation and I also had the weekend with my dad coming up. It really didn’t compare to the spendings of 2022. I decided to go ahead and track my October spendings 2023 nevertheless. In the end I decided to not include the cost for the vacations in this spending report. It would have messed it up too much.

I stuck to just tracking my own spendings. I was considering doing household spendings but first of it would have been more work and it also isn’t really comparable to last year. So only my spendings it is.

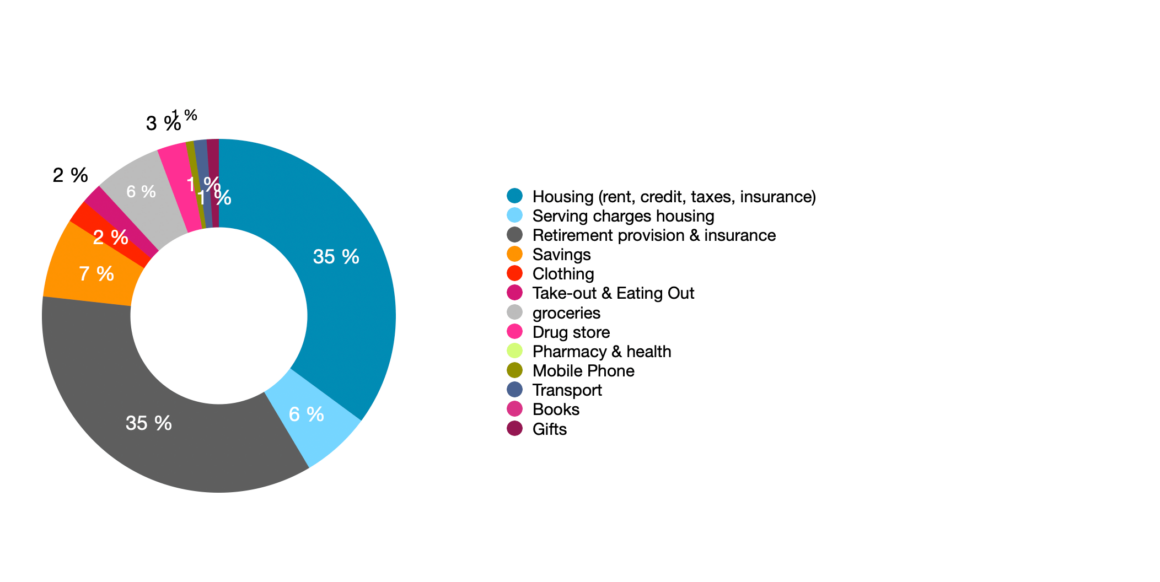

Nothing much has changed compared to last year when it comes to the big spenders. Most my money goes to insurances and retirement (35%) then for housing (35% +6%). Now please keep in mind housing is only the share I pay. It is double the money.

Compared to last year rent has gone up. This was due to the move we were forced to do. Within one year rent prices have gone up about 20% here in Berlin. And we really did’t have a choice in paying more. While I like our new apartment – it is in better shape than the one we were forced out of – it still rubs me the wrong way to spend so much money on rent. But what can you do.

The service charges housing includes all the bills that accumulate and that are paid from our joined account. So I am not completely sure about the exact amounts. And important info this also includes internet and streaming subscriptions.

Insurance spendings

It never stops hurting to look at how much I monthly pay for insurances.

I have insurances like my business insurance or my international health care that I pay annually and that don’t fall into October. My health insurance is still the highest of them all even though it slightly dropped this year. As a freelancer I have to cover that all by myself and the amount depends on my income and that has been lower than last year. But it is a lot I am paying and I really might have to look into it more closely and check if it makes sense to which the insurance company.

As a freelancer I also have to save up some money for my retirement. I do not have any employer taking care of that. I do have a couple insurances for that – not the best options but I was young. I also try to build up a portfolio to close the gap I am having for retiring. For that I have a certain amount that goes into the portfolio and is automatically invested into stocks. if that will keep me afloat during my retirement – lots hope so.

Spendings for Savings and freelance life

I like to save as much as I can. Currently that is 7% a month. This is a bit fluent. If I spend less I put more in savings. Less in December as I have all the Christmas spendings. However ever since I started full time work I have tried to put some money into savings. And I know I am a rare breed when I say I have never been in dept in my life. Very privileged. Very thankful. And while this is still true I am struggling to make ends meet recently as every day costs are rising. I had to move some money from my savings back to the account in order to not go into overdraft. Not ideal. Need to keep an eye on that.

Maybe a quick side note since I dipped into freelancing. I do have two separate accounts. And I pay myself a monthly salary from my business account to my private account. That salary is fixed (at least for a year) and if I earn more I don’t get a raise. But I also don’t get cut when freelance work slows down a bit. I try to have a steady income that is oriented on my spendings.

The savings here in the diagram are additional savings as a private person.

Spendings on Food

Compared to last year our grocery spendings have gone up from 2% to 6%, And that is only my share. We usually don’t keep track much who pays for what – it is whoever in the store does it. For October it actually is almost exactly 50:50. However it is still not quite correct as I was away for 4 days and then we spend 7 days on vacation. The food we ate then is not included in these spending. So a regular month grocery spending would be even higher. This is really showing how much prices have increased.

Additionally we are shopping less at the discounter since we are now living in an area where there are less discounters and we never come by them. Since we only have one car the husband usually takes it and if I need to get something I only have one option I can reach by bike and foot. Going to the discounter is really getting out of our way and takes much more time. However I try to do it once a month to stock up on basics.

As last year I need to mention that some of our groceries are bought at the drugstore. The drugstore carries a lot of organic foods. I get my oat milk, healthy candy, cracker and nuts, honey or at times noodles or flour.

Spendings on Take-Out

October was also a bit higher on my spendings when it comes to take out. We have been rather good about not ordering in so much but in October I was socializing a bit more since I wasn’t working full-time. The husband and I went to a brewery pub we wanted to check out and my sister and I went to a spa where we had some coffee and cake and after had a nice dinner.

I didn’t spend any money on my hobbies in October. No books, no craft supplies. However I did already started to buy gifts for my three shoeboxes I am packing for my volunteering of Christmas in a shoebox. That however still only comes in as 1%.

I think I did a pretty good job in tracking all the spendings this year. And it is also good to see that – besides the extraordinary expenses for vacation everything else is more or less the same. At least percentage wise. Overall costs have gone up by 20%. And that is not really good for the long run. Especially since I do not have a full-time project for right now and the client I have doesn’t cover the monthly expenses. So for the coming months I will dig into those savings I have.

Have you realized that prices have gone up? Do you track your spendings? How do you handle price increases? Does it make you nervous when money is tight? Do you have to take care of your retirement by yourself?

18 comments

This is a great budget deep dive– you are so responsible with your money!

I don’t feel responsible at all to be honest. But it is interesting that you think I am. Maybe I am too hard on myself

I used to track my expenses to the penny, but I stopped sometime during the pandemic. This is a great reminder to me that I should start up again in 2024. New goal for the new year!! Thanks for the encouragement to do so.

Oh wow tracking it to the penny and than throughout the year would not be something I would like to do. But once a year is a good way to get a feel.

I have to take care of my retirement savings by myself, too. It’s one of my biggest stressors since leaving full-time work. I put my entire earnings (which is not a huge amount) into an IRA. I really hope that my retirement savings accruals from before I went freelance will last me, but it seems impossible.

Reading about other people’s spending is so interesting to me. Now that we have moved, most of our expenses are higher, so I really want to get back into the habit of tracking our spending.

Yes moving can do this. Unfortunately. It’s not easy. And I hear you on the retirement thing. The money I put into the state retirement savings will maybe buy me food so not much to go with. Right now in have no solid plan but at least I’ve started. If you have the perfect solution let me.

Phew. I hear you on the raised costs of EVERYTHING. I honestly don’t know how anybody can live. I am very lucky that I also have never been in debt (something that is much more common – and less frowned upon – here in the US, but which I am still not willing to do in any capacity and luckily, we can still budget with the money we have… but man, the costs of living rises (don’t get me started on rent, food and gas prices here in CA). and rises and my paycheck does not (and we cannot even negotiate salaries at the government). It’s frustrating sometimes.

I think you’re still doing a great job keeping an eye on all the necessary pieces of the budget pie.

I hear you. It is tough right now and without trying to be pessimistic I think we are in for a long(er) run. It’s tough that you can’t even negotiate. And with your field of expertise there aren’t many option for going somewhere else, right?

As a freelancer I am trying to race prices but there is always some desperate who will do the work for less. So also tough.

Prices definitely have gone up. It’s most obvious at the has station when I pay always above $50 now but also at the grocery store or eating out. Salaries luckily went up, too so it is not a problem for us.

I feel lucky that my employer does pay retirement benefits but we do a little extra on top of that, too.

Well that is amazing that your employer has given you raises. So good. I don’t fill up our car much so I can’t say anything about gas but I see it in the grocery when I pay 100€ at the Discounter and we are only two people.

Budgeting is so much harder these days. I’ve fallen off the bandwagon of tracking my expenses closely (I did these monthly breakdowns for a few years on my blog, but it got so tedious!) and it shows in the way my budget has NOT been working for me. I recently reworked my budget to suit my needs and we’ll see if it helps!

I would not want to monitor my budget this closely every month. So much work. But once a year it’s interesting and helpful. I am hoping your new budget set up is working for you.

I find prices have really gone up and the cost of living keeps rising.

This post so interesting – thank you for sharing. I am usually good at sticking to a budget and find I’m being more mindful when it comes to shopping.

Yes prices have been so steep lately. I am also minded um about shopping. Not always easy. Glad you are having it well handled.

This looks like the ideal budget! American’s are told to spend 1/3 on housing but most end up spending more than half. Good on you for so much investment.

Veronica Hanson recently posted…3 Best Hotel Chains to Earn Status

Thank you Veronica. It is the same here in Germany and landlords don’t often rent you an apartment/house if it is more than 1/3 of the income. It is becoming a problem here though because housing costs went through the roof.

This is very interesting. I live in one of the most expensive states-New Jersey- so we have to watch our money. Both my husband and I have full time jobs but a point of tension in our relationship is spending- he likes to spend, I like to save or wait and spend on travel down the line.

We used to do the budget every month but fell off the wagon- need to resume.

I also like to keep the money and my husband is more prone to spending. I think we both adapted a bit to the other so we meet more in the middle now. But just me I would probably spend less and buy more sales and promotions if I need it. Luckily it’s rarely something causing tension though.