For the past two years I have been tracking my October Spendings. I am wy too lazy to do it all year round but one month to see how things are going is a good exercise. And it is odder for a NaBloPoMo posts. Win win, no? This October was really low key and I have a feeling I didn’t (have the chance) to spend much but lets have a closer look at the October Spendings 2024 – I maybe mistaken and want to cry at the end of this post.

I will again only track my own spendings. This way it is much more comparable to the past two years.

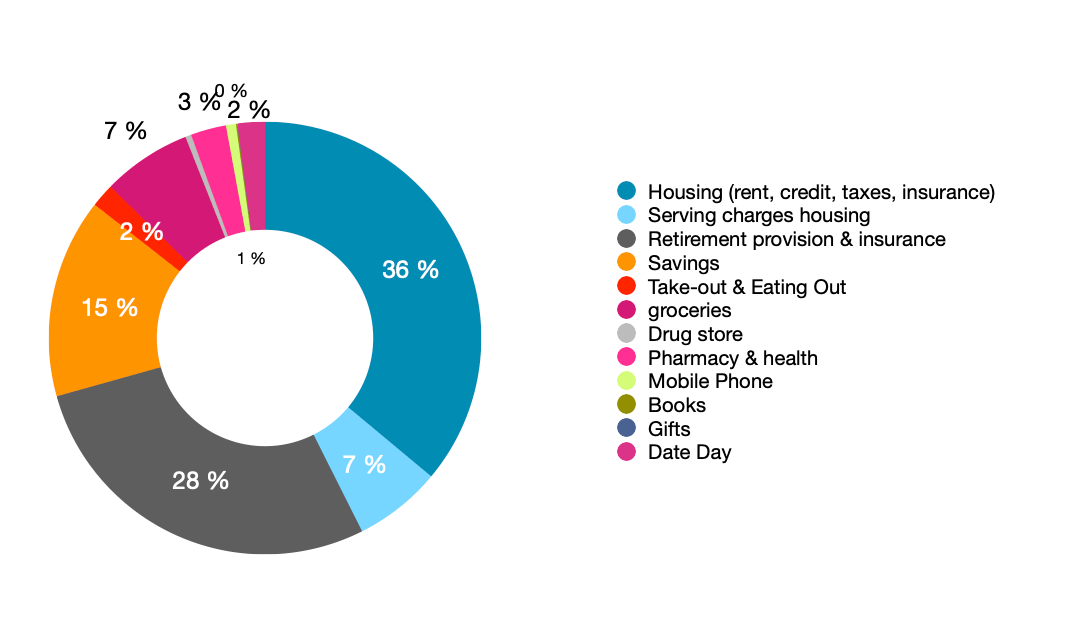

Percentage wise it looks a bit different this year because I have overall spend 400€ less than in 2023. But the big spenders are still housing (39%+7% – same amount in actual money though) as well as insurances and retirement (30% -5% and in actual money about -200€). Now please keep in mind housing is only the share I pay. It is double the money.

The serving charges for housing include the utility bills, energy, heating as well as internet and streaming services as well as car stuff. It is paid from our joined account and I just transfer a certain amount to that account on a monthly basis. Again this is only half of the actual costs as the husband does the same. As for the energy bill it is a prepayment we are making monthly and by the end of the year we receive a final bill. Last year we have been overpaying and received 500€ back. We could have adjusted the monthly payments but opted for overpaying and then getting a refund later. With interest probably not the smartest idea but in case we use more energy or prices go up we are not getting a surprise end of the year.

Early summer we have canceled the Netflix service and are now having Apple TV, Amazon Prime, Disney and Wow. Disney is part of the husband’s cell service as a signup offer so we are paying a very good price here. The Wow service was also a promotion. Which we will cancel in the next couple of moth probably.

Insurance spendings

It never stops hurting to look at how much I monthly pay for insurances. I have insurances like my business insurance or my international health care that I pay annually and that don’t fall into October.

My health insurance is still the highest of them all even though I was able to reduce it quite a bit by changing the health care insurance. As a freelancer I have to cover that all by myself and the amount depends on my income. Since this is a rather low income year for me that explains the low rate. However I am rather certain that once taxes are done I have to pay to meet the right amount of rate. And government has just decided to raise health insurance prices by (I think) 1.5% and since we are childless we pay extra. Sigh… I should be more sick but that is not how the system works. And my monthly rate is almost as high as the migraine medication I need so I guess it’s a good deal. It still hurts.

As a freelancer I also have to save up some money for my retirement. I do not have any employer taking care of that. I do have a couple insurances for that – not the best options but I was young. I also try to build up a portfolio to close the gap I am having for retiring.

Spendings for Savings and freelance life

I like to save as much as I can. Currently that is 15% (+8%) a month. I am surprised about the percentage to be honest. Half of it is automatically transferred into a portfolio and then automatically invested in certain stocks and ETFs. I have doubled that amount compared to last year (which explains the higher percentage). I hope that will keep me afloat during my retirement – let’s hope so. I also save the same amount into an emergency fund. It is a bit higher currently as I have to fill that fund up after being unemployed earlier this year. Once I hit a certain amount in the emergency fund I keep it at that and move more into the portfolio. Or maybe splurge and do something.

I know I am a rare breed when I say I have never been in dept in my life. Very privileged. Very thankful. And while this is still true I am struggling to make ends meet recently as every day costs are rising. I am not feeling as desperate as last year – even though more money is spend. I guess we are getting used to everything even higher prices. Sigh.

Maybe a quick side note since I dipped into freelancing eight years ago I do have two separate accounts. And I pay myself a monthly salary from my business account to my private account. That salary is fixed (at least for a year) and if I earn more I don’t get a raise. But I also don’t get cut when freelance work slows down a bit. I try to have a steady income that is oriented on my spendings.

The savings here in the diagram are additional savings as a private person.

Spendings on Food

Compared to last year grocery spendings have remained the same on my end with 7%. However the husband often picks up stuff on the way home because he has a car. He also doesn’t care about prices and will not buy on coupons and bargains. It drives me nuts but it is his personality. I assume he has spend about the same amount maybe a little more. I try to do one or two grocery runs to the discounter a month to stock up on basic and canned things. It really does save so much money. But I always have to see when the car is available as the next discounter is 6.5 km (13 min) away. In October that was only one because plans changed. I ended up order a food delivery.

As last year I need to mention that some of our groceries are bought at the drugstore. The drugstore carries a lot of organic foods. I get my oat milk, healthy candy, cracker and nuts, honey or at times noodles or flour. However this October we only bought drug store items hence the low number. But we are running very low on all the above mentioned items.

Spendings on Take-Out

I have used the To-Good-To-Go app three times this month. The best haul was a pick up for 3€ at the hospital cafeteria where I gotten two quiche, 6 rolls and a mango lassi. I will try to do this more often as it is tasty and provides me with lunch and dinner options when the husband is in the office. Also it’s a nice walk through the forest for about 2.5 km one way.

The higher bill was when having lunch with my dad at the Pakistani restaurant. He forgot his money otherwise I would have been invited. I may get the money back but if not it’s also fine. It was a nice lunch. And I had only eaten half to take home but then I forgot so dad ate it and enjoyed it.

Additional Spendings

I did spend money on two kindle books that were on sale. I also bought a wreath form at the craft store for my upcoming advent wreath.

And then I spend some money on additional magnet frames for my picture wall. I have yet to find the art work but they were on sale during prime days and I figured I rather save 20% right now because I need them anyways.

I think I did a pretty good job in tracking all the spendings this year. And it is also good to see that costs are more or less the same compared to last year. Costs have not significantly gone up. At least not in the private spendings. Business wise I had to invest more in software but that is not part of this tracking.

How are you handling money right now? do you need to pinch penny or I it going alright for you? Have prices increased compared to last year or plateaued at your end? Do you track your spendings? Does it make you nervous when money is tight? Do you have to take care of your retirement by yourself? Who is handling money in your household?

22 comments

very interesting about health insurance. It’s so important and it is expensive. fortunately we have it covered by my work.

I track spending monthly and do a review yearly. It keeps me accountable about where we spend the money, whether my spending habit reflect our values. I use google sheet to do the tracking. Now given the incidence with the bank, I may also track/update each account’s balance.

I am too lazy to track monthly.

But I check my accounts monthly because I have to do taxes on a monthly basis so that’s a good habit.

I’m VERY impressed with the amount you’re putting into savings! I think the #1 thing you did for your financial security was to not have kids. Kids will keep you poor! We’re definitely pinching pennies with a kid in college, and another one going to college in a few years. My husband and I had kids later in life, and didn’t manage our money well when we were younger, so we will be working for a long, long time.

I’m also impressed with your grocery spending. That seems low to me! My son will be home for a week at the end of this month, and our grocery bills will skyrocket then.

This is only have the groceries we buy. The husband is often picking up stuff on the way home. But food is not as expensive in Germany as in other countries I’ve realized that.

Haha yes not having kids is most likely a good thing when it comes to money.

I was surprised about the amount I put into savings and am not sure why so much is left when a few ok th ago I had nothing and lived from savings…. Because I haven’t changed anything really.

Honestly, I haven’t noticed much difference at the grocery store because we always spent a ginormous sum. *shrug* But my pets are so expensive! Sometimes I wonder what our savings account would look like if we had never gotten pets!

The pets are expensive from what you share. Definitely an investment but they also bring you so much joy. Other people travel or go to the theater and you have pets.

Oh, I feel for you and totally understand how hard it is being a freelancer, and having to pay all your own insurances for health. While I love being freelance it was crippling because each month could be famine or feast. Whether I got paid on time, or not. Then you ad on everything else in life, and I wonder how anyone copes doing freelance work anymore.

Bravo to the fact you still find money to save. You must be doing something right.

Thank you, Alexandra. It’s not always easy and there are indeed some month that I need to take a deep breath and believe that everything will work out. Fortunately, I managed to run the show for eight years now. I don’t know what I’m doing right but I’m glad I do. What are you freelancing in?

I read this as we discuss getting take out sushi tonight because we are too lazy to cook. It’s Friday, both our kids are home and our eventual to be daughter-in-law will also be coming by, so we want to just spend the time together as a family. I know we could cook but I did the majority of that this week and I’m tired. Lame I know.

I’m on a work break, thinking about retirement (and maybe consulting again); our home is also in need of renovations too. We have a very senior dog, still have a child to finish up university – and would love to travel more. Groceries are definitely more expensive, but I do have an app that highlights sales so I can time shopping accordingly, and I am big on loyalty points.

I am a fan of loyalty points to, but it’s a moot point when only one person in the household is dropping by it. Well I guess half is better than none. I hope you enjoyed your sushi. I think money as well spent when you have more time with family. And not being in charge of cooking as a form of self-care and that is important too.

I have the Too Good to Go app, but have never used it. It seems like it’s mostly things I don’t want, like muffins or whatever. Your options sound good though!

We handle our money like you do. I have my account, my husband has his account, and we have a joint account for bills. I put money away every month for savings, but not as much as you do, your numbers are impressive! We have a weird system that works for us regarding groceries. I pay when I cook (or if my daughter cooks), so that’s Mon – Thurs. My husband takes us out for dinner every Friday (leftover from lockdown phase, we were getting takeout to help the restaurants and to keep ourselves from going crazy with boredom), and he buys groceries and cooks on the weekends. So I buy groceries for 4 days, he pays for 3, but going out to eat is more expensive, so probably it’s close to even. We don’t try to keep track of who is spending what, I think that would drive us both nuts.

As Jenny and Engie said, kids and pets are so expensive. I miss my sweet Mulder so much, but yeah, I’ve been putting more money into savings since we finished paying for his cancer treatments. :( And our daughter is an adult, so while she lives with us and we pay for her food, she also pays a couple of bills around the house (instead of paying us rent), and she buys all of her own things and is out of college. But wow, those first 22 years were a LOT of money. My brother doesn’t have kids, and his cats are thankfully young and healthy, and he has managed to save a lot more than we have, and he makes about the same amount I think.

Insurance is interesting, I never know how different countries handle it. Here in the US, it’s mostly through your employer (is that true in Germany too? And you pay it because you are self employed?). There is a government marketplace where you can purchase insurance, and I think it’s like what I understood from your post, if your income changes in the middle of the year you might end up owing a bunch when you do your taxes. But I’m not clear on it, because we’ve always gotten ours through our companies. Right now we are lucky, my husband’s employer is paying 100% of the premiums for both of us. At my company, they would pay 100% for the employee only, but it would be more for a spouse or family. To cover the three of us would be about $1,400 a month, so I’m really glad we have free coverage through my husband’s job. My daughter gets hers through her work, she is too old to be on our plans. Hers isn’t as good as ours, she has to pay, but it’s not terrible. It varies a LOT from employer to employer.

Sorry for the super long comment!

The Too Good to Go app needs a bit of experimenting with your local places. I often freeze the cake/muffins and stuff and pull them out when I need treat or have company over. And you can filter in the app a little – it’s been getting much better now where you can include dietary requirements.

As for the insurance… yes if you are employed in Germany the employer is taking care of half of your social insurances that include health care, nursing care insurance (obligatory in Germany and will be paid to health care service who then distribute to the state, for childless people the percentage is higher the argument being no one will take care of us when old) a certain amount goes into the pensions fund, unemployment insurance and casualty insurance (for your workplace). As a freelancer I have to cover all that on my own. While unemployment, pension and casualty are not mandatory the healthcare and nursing care insurance is. However companies hiring me usually have it in their contract that I have some sort of pension plan (it’s something to do with a complicated system I can not explain) and when working in bigger company they require a liability insurance. So it is a lot. On top I also have an occupational disability insurance that I started before migraines and depression were diagnosed. No carrier would give me that now so I am keeping it. Part of the money will be paid if I die to my next of kin.

It is all very complex and complicated but I guess it is part of adulting and being self employed. I have some sort of commercial training as it was part in my education for advertising so that helps.

It is also possible to insure your kids and partner in a “family insurance” for healthcare and we have done that until we were too old.

I was very surprised with the amount of savings I am currently able to put away and can’t really explain why that money is left over. I guess it became a habit and then it was suddenly possible. As sad as it is that Mulder is gone saving up a bit must feel nice though.

We are in a slightly better position than last year with our son working now, and our daughter will likely be in grad school next year so needing less money. Our grocery budget is way down with the kids not here, and my husband has been traveling a ton for work, and I guess that means at least work pays for most of his meals. We need to do quite a bit of work on the house, so still trying to spend less.

I just looked up the Wow streaming service – is that mostly German programming? We are in the process of reworking our cable and streaming stuff because what we’re paying now is ridiculous.

No pensions here either, so we have to pay a lot of attention to savings and investments.

Yes the wow thing used to be a paid cable channel but is now trying to position as a streaming service. It’s going okays for them I think. But they do have couple shows we were interested such as Game of Thrones, westworld and such.

I bet having to feed only 1.5 people is easing up some grocery budget. But then a house will eat it up. I guess having kids is a whole energy struggle for budgeting. And right when you are done here come retirement and what now…

I keep track of most things money but my husband does the investment accounts. We always talk about it but he will make sure everything stays on track. Groceries over all got more expensive than last year but I think the last couple of months have been fairly stable. We don’t have to pinch pennies since my husband’s job lets us live comfortably. Both of our retirements are through our work but we do have some extra investments, too.

That sounds like you are on solid grounds. That is so good and such a relief. I am wondering though does the retirement through work would be enough? As you probably know in Germany you couldn’t live of it really.

Woah! How did I miss this. I love a good finance/budget post! Before I comment, I want to add to J’s comment re insurance. Like she said, if we are employed, our employer usually pays part of our premium. For me at my last job, I was still paying about $200/month, and my employer was paying the rest, which was about $600 (so $800 total). To pay on my own once I quit, I would have had to pay the entire $800. However, like she said, we also have subsidized insurance, but it varies by state and I did look into it. If you make ~ 60k, you would have to still pay about $500/month and then it goes down or up from there depending on your salary, and you can owe (or get money back) at the end of the year if your estimate was off. I ended up going with private insurance, because it was cheaper, and it is about $250/month.

I do track my expenses every month, and have an October wrap up planned to go live soon! However, I can give you a spoiler, I am spending much less now than when I was working (like basically about half) despite the fact that I am on the road more and eating out more etc. However, I am going to have to do some electronics upgrades (new computer – ouch) this month so the numbers will go up a lot in November!

Also, I used to do what you do to an extent, where money got automatically transferred and invested. Now that I don’t have a salary, I do it a little differently. I should write a post about this, but I have all my credit cards due on the 4th, and on the 1st I transfer money from a high yield savings into my checking to pay for all of the bills. This way I can maximize my investments and not have cash just sitting there doing nothing. I have no kids or partner, so it is a lot easier to keep track of!

Thank you for explaining the US system a bit more.

I could also get private insurance. However they start with lower prices and then raise them annually. And once you pass 50 or 52 you are not allowed to go back into public health care. My husband has private healthcare for probably a decade and while he is paying a little less than I do it will rise and he has to prepay all procedures. So it’s a consideration to take. if I had to pay my migraine medication on a monthly basis and then have to file for refund at the end of the year it would be a lot of money. I rather keep that and get interest.

I probably could have mentioned that my emergency fund is not in my regular account but an accessible savings account with good interest rate. My checking account is loosely holding the amount of my salary and tends to go towards 0€ by end of the month.

I really appreciate the many money posts in the community. I think it is very important to talk about it and educate ourselves about it. Specially as women.

I am not pinching pennies at this point, but I do want to move to a two-bedroom apartment next year and that’s going to really affect my budget. Housing is so expensive!

You save so much money and that’s really great! I think it’s smart to give yourself a salary and put away any overages into savings. That way, you don’t feel the pinch during the lean months but aren’t overspending in the not-lean months. Very smart!

It’s definitely a very good practice. When I started freelancing I had a serious sit down with myself and made some rules. This was one. Another one was not eating at the desk. Not working in pyjamas.

It does help that I have a harder time on spending money on myself then saving. Yesterday I pondered if I should order 2.50€ ink cartridges in pink because I always wanted them. I did not. I am cheap and mean to myself sometimes.

I think you are also very smart to start budgeting now and getting a feel for what it would feel like living in a two bedroom apartment.

As you know, I love the budget posts because it’s so interesting to me how different people handle their money.

We have a bit of a unique situation, because we only have one salary (mine) but get extra funds through investments/trust money. We do track our spending every month and I am also one of the lucky people who never had any debt. I would worry myself sick if we did.

We’re doing fine financially, although I need to add that we’re not very ‘spendy’ people and I do try to save money where I can. Life definitely has gotten more expensive! I just had a burrito for $20 for dinner the other day. A simple burrito that to cost half a few years ago!

I hear you are on the money spent on food. The other day the husband was away and I decided to order some sushi for myself and I paid €40 can you believe it? I mean, I could probably have ordered a little less but still crazy. I bet it’s double hard if you only have one salary to rely on.

Congrats on never being in debt that’s definitely something to be proud of. I don’t know. I probably would very sick too.